Published on

July 16, 2026

Sierra Ventures' CXO Advisory Board, one of the longest-running and most active networks of enterprise leaders in the industry, provides rare insight into how Fortune 2000 and growth-stage companies are actually deploying AI. We surveyed members of this network, alongside our Engineering & Product Leaders Council, and conducted interviews for our CXO AI Insights podcast.

What we found: the experiment phase is over. What separates winners from the rest is no longer capability. It's operationalization.

The Bottleneck Has Moved Up the Stack

The conversation inside the enterprise has fundamentally shifted. It is no longer "can the technology do this?" It is now "can we change how we work to take advantage of it?"

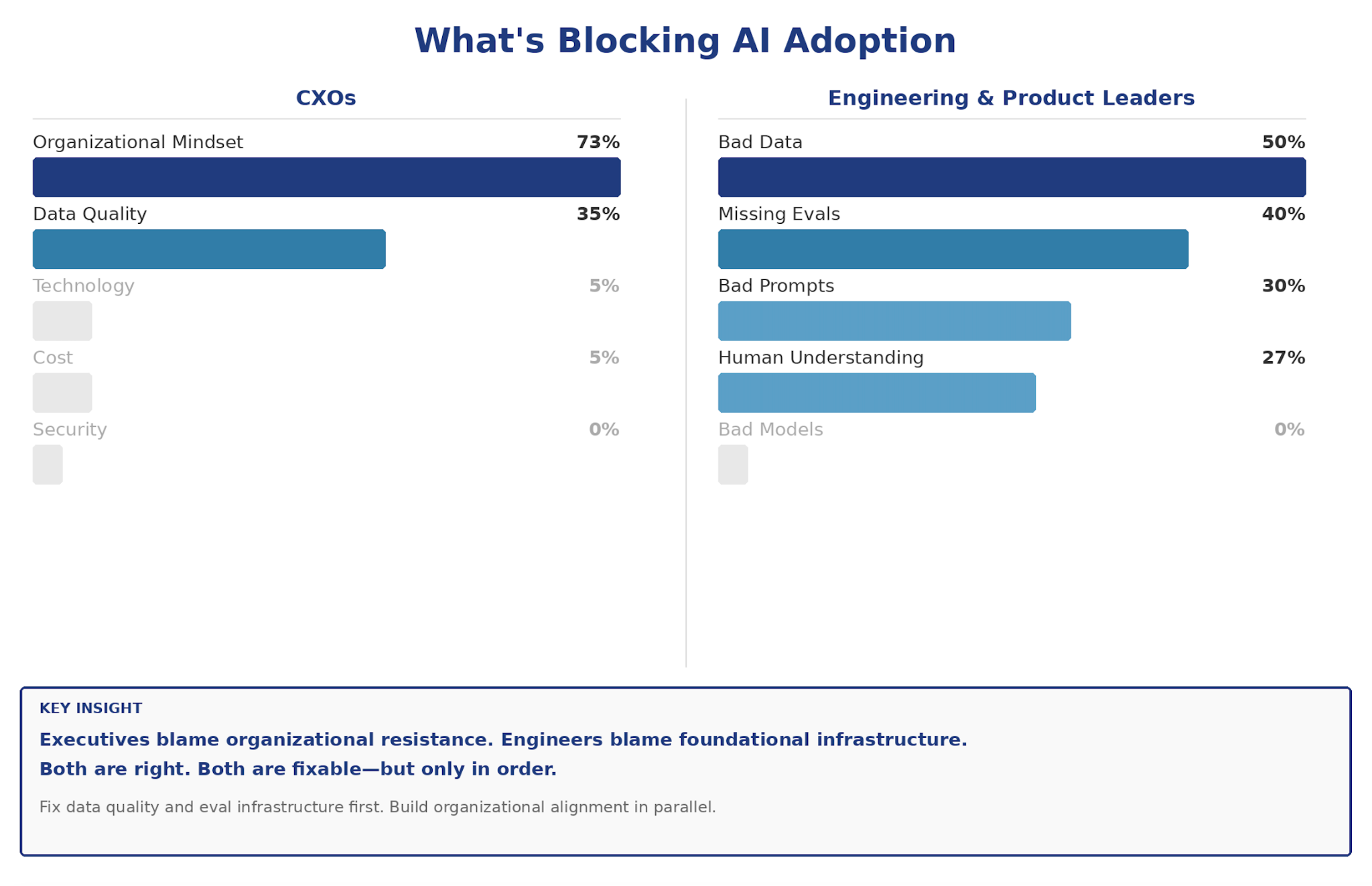

73% of CXOs identified organizational mindset as the single biggest barrier to adoption, far ahead of technology, cost, or security. Not a single respondent blamed the models themselves.

At the engineering and product leader level, the picture is equally clear but different in flavor. Among product and engineering leaders, bad data is the most common blocker at 50%, followed by missing evals at 40% and poor prompting at 30%. Again, zero respondents pointed to model capability as the issue.

What this reveals is a critical insight: technical blockers are fixable. Organizational ones compound them. A team can solve bad data. They cannot easily overcome reluctance to trust non-deterministic systems, legacy workflows designed around human decision-making, or an org chart that hasn't been restructured for AI-native operations.

The constraint on AI adoption has moved decisively up the stack. The foundation is still wobbly. Teams are working through data readiness and evaluation infrastructure. Without clean, structured data and production-grade eval pipelines, even strong models fail. But above that sits something harder to fix: organizational inertia.

Adoption Is Universal. Autonomy Is Rationed.

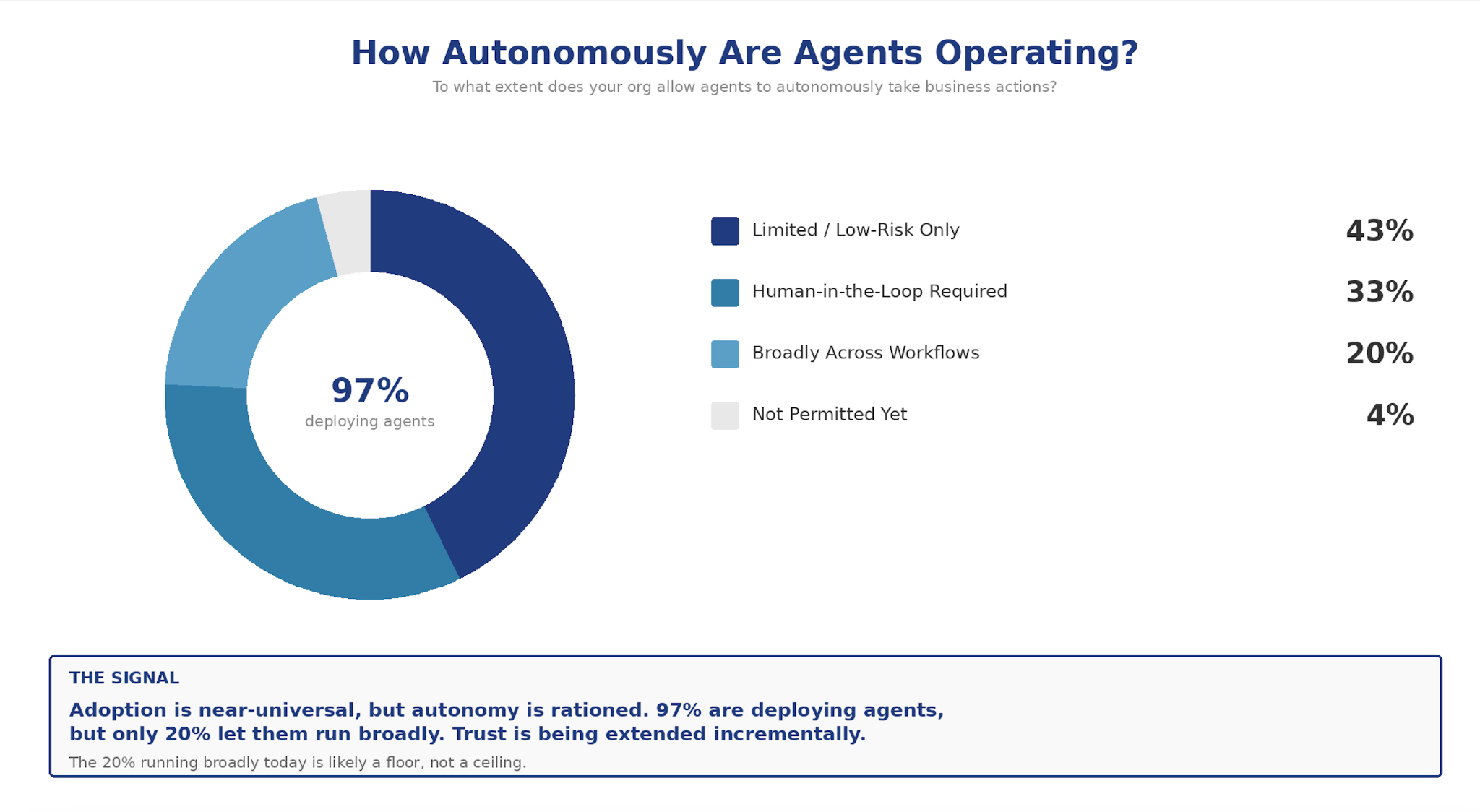

Here’s what dominance looks like: 97% of engineering teams report deploying agents in some capacity in 2026. But that number obscures the real story.

43% limit agents to low-risk workflows, 33% require human-in-the-loop approval, and only 20% allow broad autonomous deployment. Fully autonomous systems remain rare. The direction is clear: teams are moving forward, but not without guardrails.

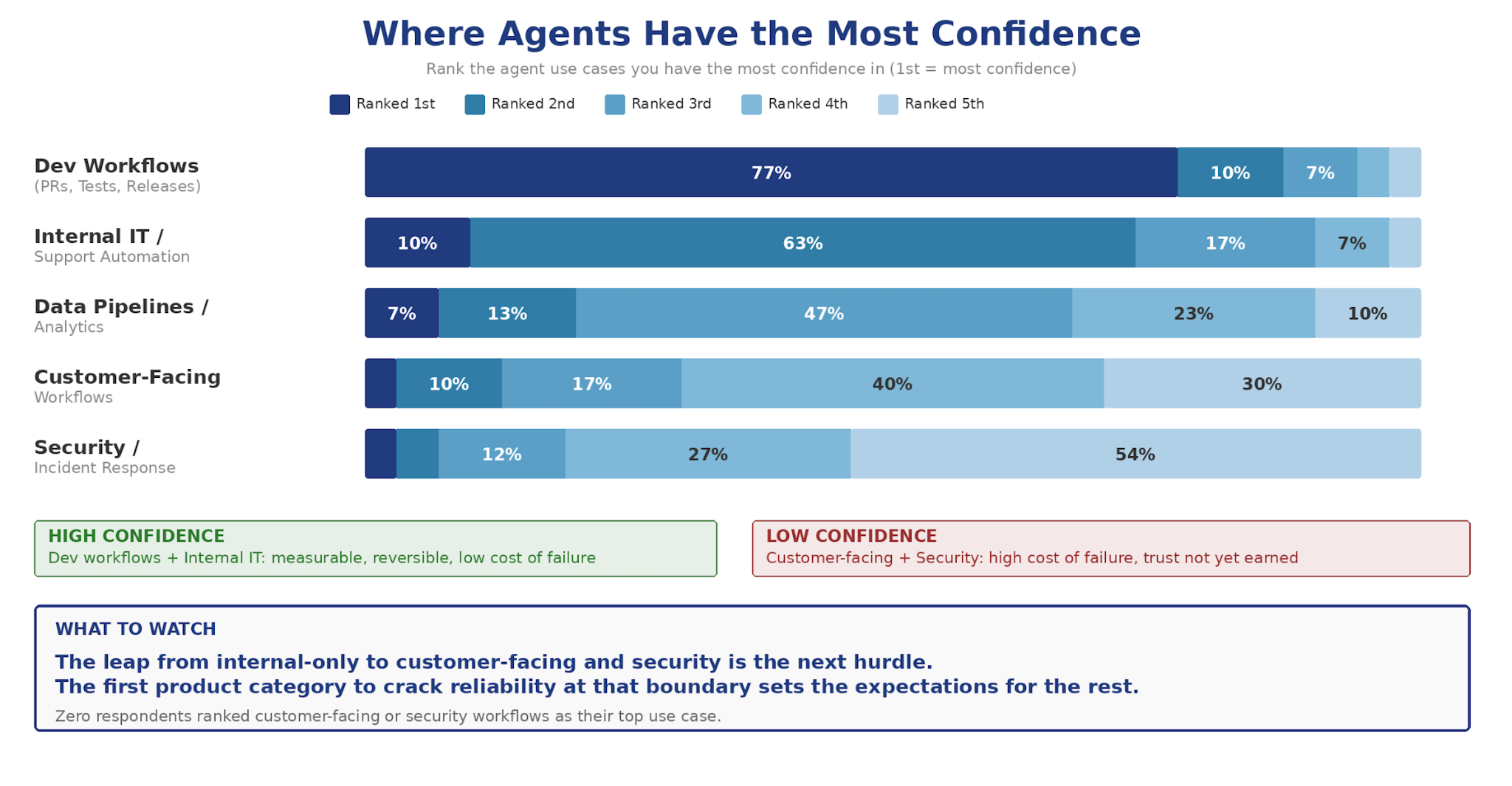

Trust is not evenly distributed. Teams have the highest confidence in environments where outcomes are measurable and reversible:

- 77% rank development workflows first (PRs, testing, releases)

- 73% rank internal IT and support automation in their top two

- Zero respondents ranked customer-facing or security workflows as the top use case

In these higher-stakes environments, the cost of failure matters more than the success rate. This is not risk aversion. It is calibration.

Organizations understand where they can afford to learn, and where they cannot.

This pattern will likely accelerate. Several major agent launches arrived after this survey closed, making the 20% running broadly today more of a floor than a ceiling. But the larger trend is about trust-building. The next 24 months will separate organizations that can prove reliability in controlled environments from those still stuck in pilot mode.

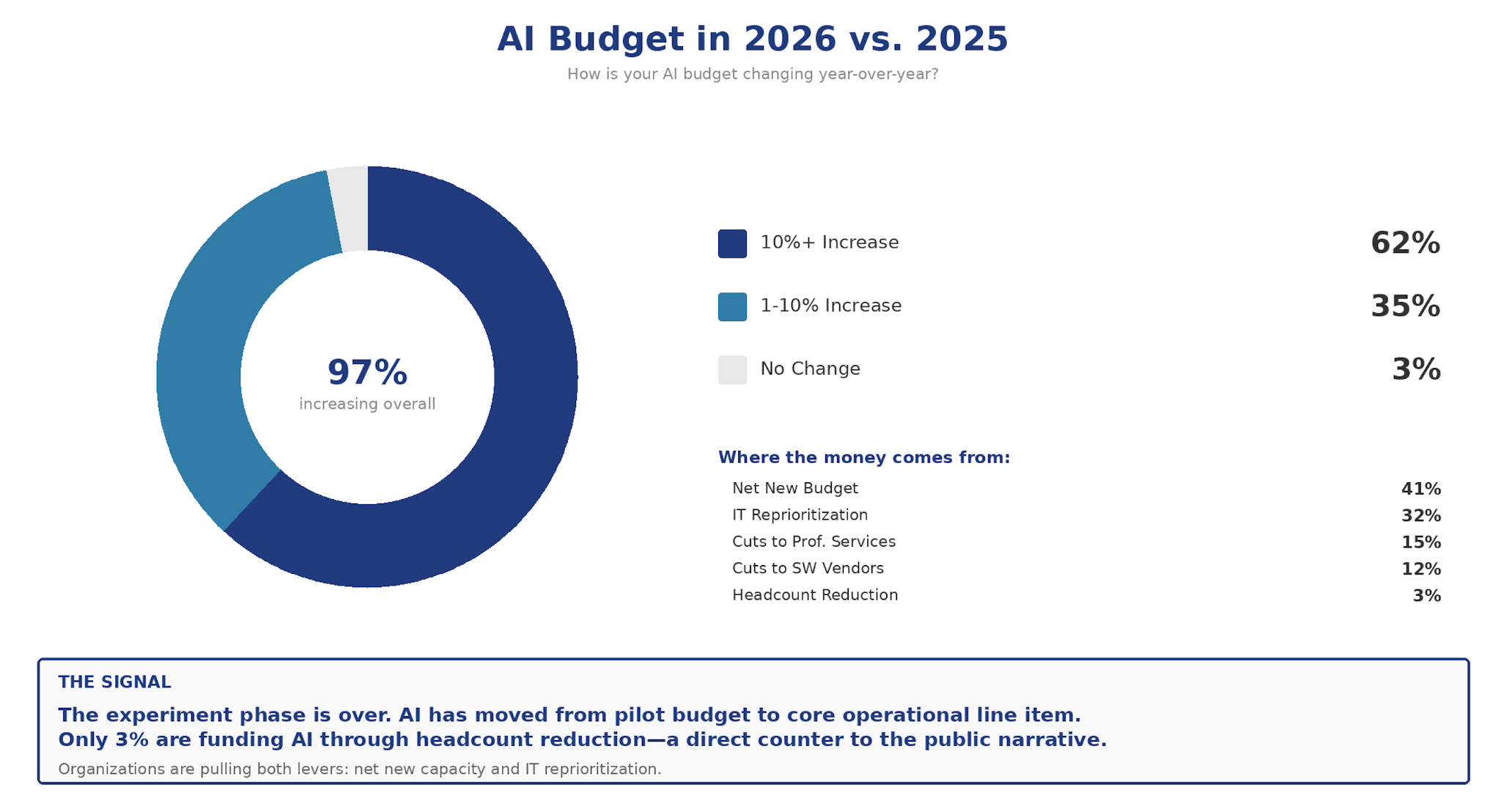

Budget Growth Masks the Real Shift

62% of CXOs are increasing AI budgets by more than 10%, and 97% are increasing overall. On the surface, this looks like explosive growth. But dig into where the money comes from, and you see something different: 41% cite net new budget, 32% cite IT reprioritization, 15% cite cuts to professional services, 12% cite cuts to software vendors, and only 3% cite headcount reduction.

The experiment phase is genuinely over. AI has moved from a pilot budget to a core operational line item. But the funding picture tells you something else: organizations are not choosing between growth and efficiency. They are pulling both levers. They are adding net new AI capacity while reorganizing existing IT spending. They are not mass-firing people and rebranding it as AI-driven gains.

Where AI Is Delivering Real ROI

Engineering and operational automation are the clear leaders. One team replaced the entire IT support footprint of 1,800 engineers with a homegrown Cloudflare Workers build. Code generation, SDLC automation, testing, PR workflows, MTTR on support tickets, contract and vendor management—these are structured, measurable, and stacking wins.

Customer-facing applications have underperformed so far. Revenue impact from AI remains a 2027+ story for most of this group. Right now, this is an efficiency play, not a revenue play.

The Market Gaps Driving Build Decisions

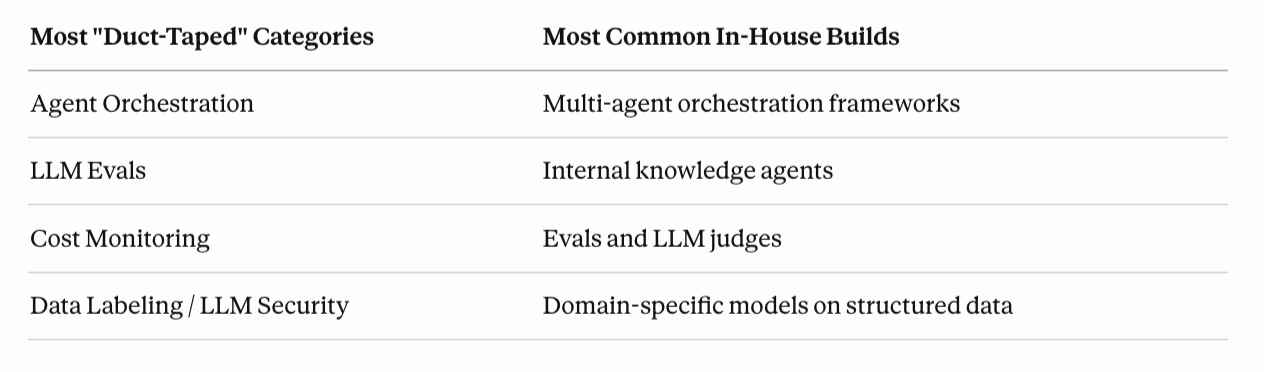

In several critical areas, organizations have stopped waiting for vendors to catch up. They are building internally. Agent orchestration, evaluation pipelines, and internal knowledge agents are increasingly homegrown.

Why? Agent orchestration and LLM evaluation are the least mature parts of the stack. No vendor solution consistently works at a production scale. The gap between frustration and a viable product is where the startup lane opens.

Most "duct-taped" categories:

- Agent orchestration (far and away the most cited). There is no good standard. Every team is wiring together its own multi-agent framework with no durable tooling underneath.

- LLM evals (a close second). The problem is not awareness. It is that systematic, scalable eval infrastructure does not exist for most teams, particularly for domain-specific tasks where generic benchmarks are meaningless.

Most common in-house builds:

- Multi-agent orchestration: Teams are rolling their own frameworks because nothing on the market meets their production requirements.

- Internal knowledge agents: Slack bots, internal wikis with LLM interfaces, analytics agents on top of proprietary data warehouses. Almost universally homegrown because vendor solutions cannot access internal data without significant custom integration work.

- Evals and LLM judges: Domain-specific evaluation needs cannot be addressed generically. Multiple organizations have built LLM-as-judge pipelines for their specific use cases.

The Tooling Picture Is Solidifying

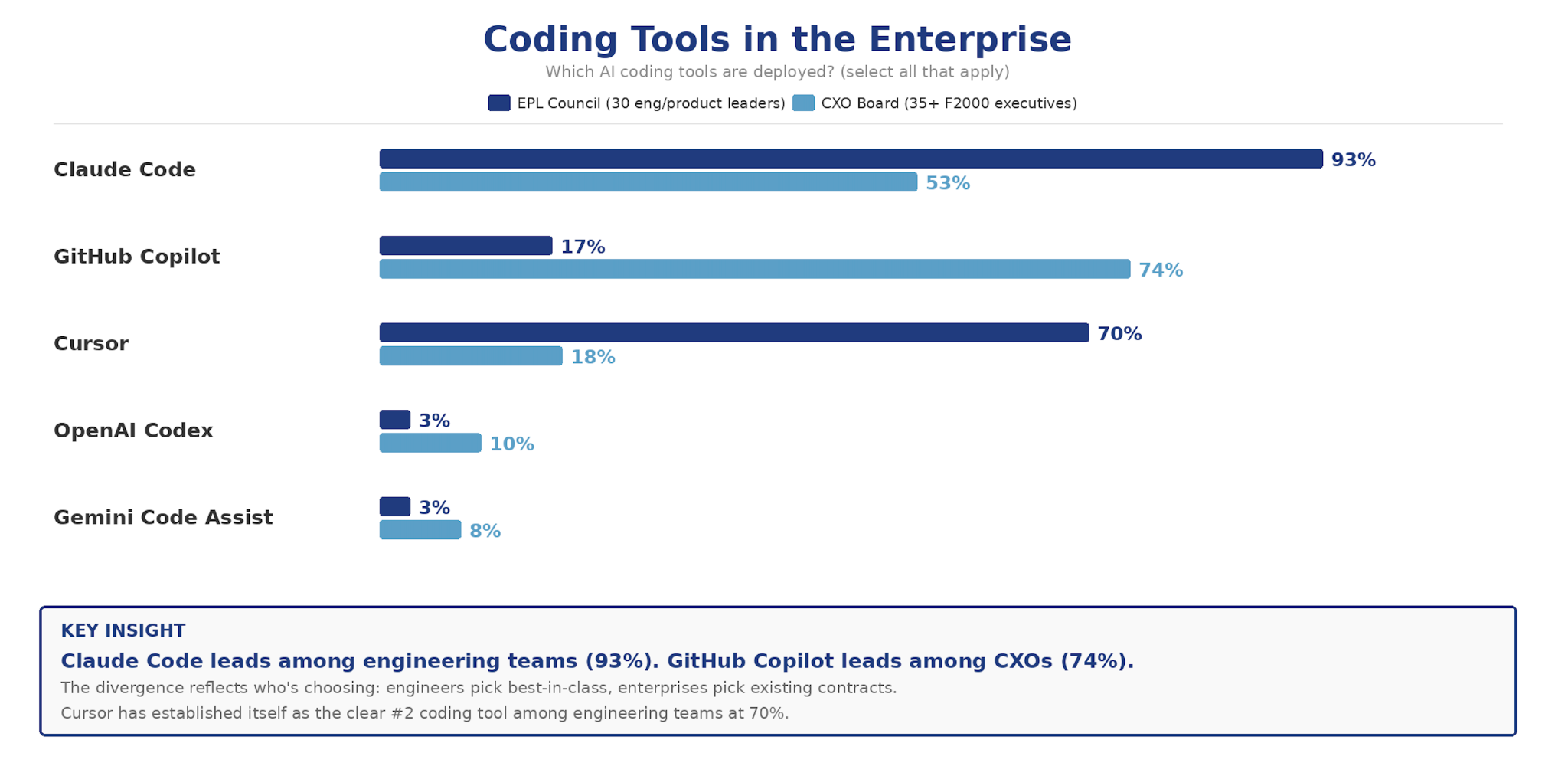

At the coding layer, Claude Code dominates at 93% of engineering teams, with Cursor as the clear #2 at 70%. Among CXOs, GitHub Copilot leads at 74%, driven largely by existing Microsoft and enterprise agreements, with Claude Code close behind at 53%. At the enterprise level, the model layer tells a closer story: Microsoft leads at 41% (existing agreements + Azure relationships), but OpenAI and Anthropic are nearly tied behind at 24% and 22%, respectively.

Claude sits at the center of both the coding workflow and the primary model layer. This is a new structural fact for 2026.

The Hype vs. Reality Gap

Adoption is accelerating, but expectations are moving faster still. Productivity gains are real, but headcount reductions attributed to AI largely are not—at least not at the scale publicly claimed. Several board members called out "AI washing" directly: restructuring and over-hiring corrections being rebranded as AI-driven efficiency. What's changing is leverage, not headcount. Teams are shipping faster, covering more surface area, and increasing output, without fundamentally changing team size. These misalignments are shaping critical decisions: how companies invest, how they plan, how they measure success.

Enterprise Readiness and Integration Reality

The complexity of layered systems, regulatory constraints, and unstructured processes makes full agent deployment far more involved than vendor pitches suggest. Most organizations are still in trust-building mode, and enterprise environments will take longer to mature.

Similarly, systems of record entrenched in enterprise workflows will not be displaced in the near term. AI will layer on top, not displace from below—switching costs are structural, not just financial. The capability will get there. Disruption is coming. But the timeline the market implies is compressed.

What Separates Winners From the Rest

Across both CXOs and engineering leaders, one pattern emerges consistently: The companies that move fastest from adoption to advantage are not the ones chasing the next model release. They are the ones investing in data pipelines, eval infrastructure, and organizational enablement.

Further model improvements will not close the value gap for most organizations. The teams that win in 2026 will be the ones that invest in the infrastructure required to operationalize AI—data readiness, evaluation frameworks, organizational alignment, and workflow integration. Not the ones waiting for the next SOTA release.

The moat is built on outcomes, not tools. Tools are available to everyone. What compounds is what you build with them.